Scope 3 emissions could soon become mandatory as they represent over 75% of the total GHG gas emissions of a company. Hence, it is imperative that organisations start strategising for Scope 3 emissions measurement.

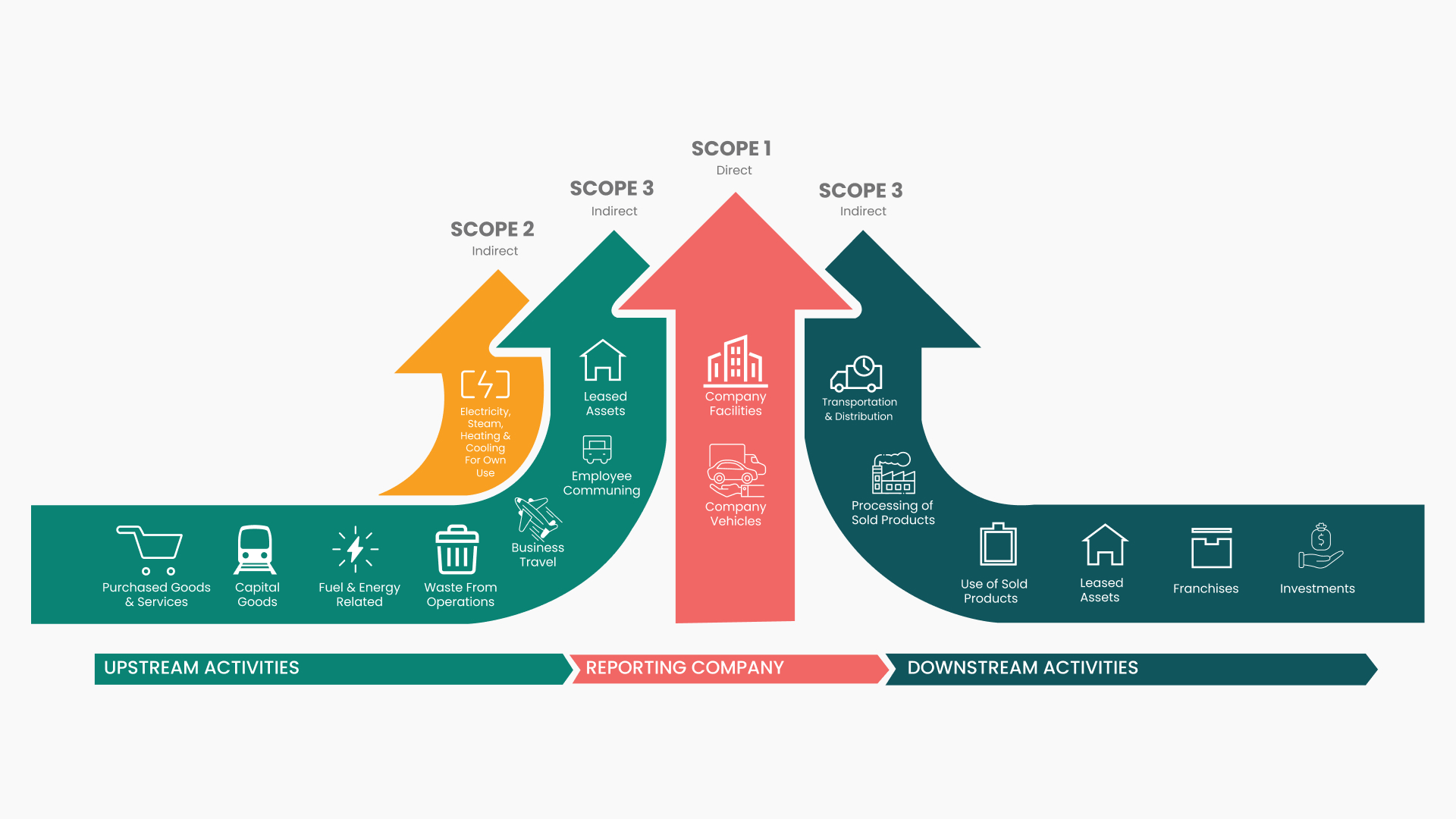

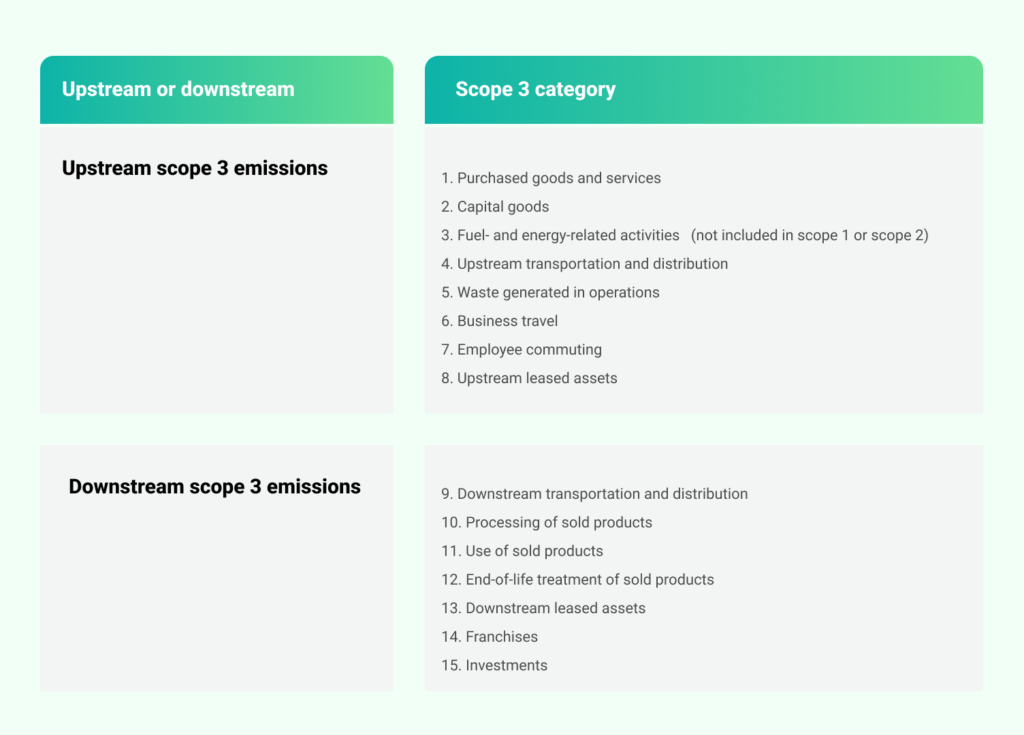

Scope 3 emissions have become a critical focus for companies as they realize that these indirect emissions, often outside their direct control, constitute a substantial part of their overall carbon footprint. According to a CDP analysis, Scope 3 emissions can account for an average of 75% of a company’s total greenhouse gas emissions. Managing Scope 3 is particularly complex, given its 15 sub-categories spanning both upstream and downstream activities, making it the most significant—and challenging—area for companies to address.

Enterprises are rising to the challenge, with CDP data showing that 92% of emissions reported by European companies in 2022 came from Scope 3. Monitoring and reporting of Scope 3 emissions are becoming increasingly common.

This blog will explore the 15 types of Scope 3 emissions across upstream and downstream activities, the challenges they present, and strategies for reduction.

What are Scope 3 emissions?

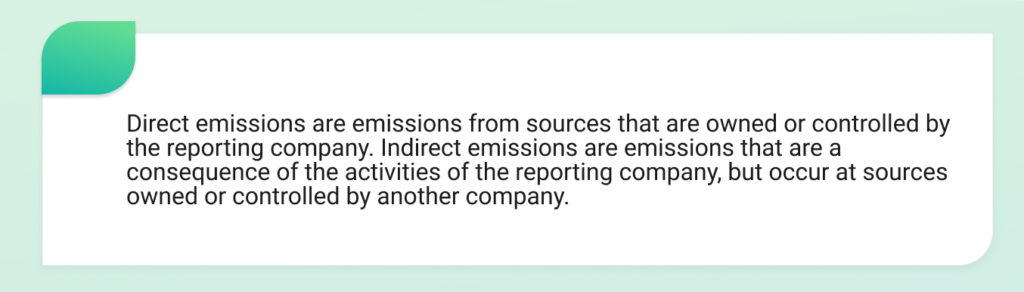

Scope 3 emissions refer to indirect emissions in the company’s corporate value chain. These emissions occur from sources owned or controlled by entities beyond the direct control of the organisation. These emissions occur at different levels such as materials suppliers, third-party logistics providers, waste management suppliers, travel suppliers, lessees and lessors, franchisees, retailers, employees, and customers. All activities that contribute to emissions but are not the result of activities under direct control of the company operations fall under the category of Scope 3 emissions. And these emissions occur in both upstream and downstream activities.

Scope 3 emission categories

Scope 3 emissions include 15 categories, which are further divided on the basis of upstream and downstream activities. The Corporate Value Chain (Scope 3) Accounting and Reporting Standard by the greenhouse gas protocol provides detailed guidance for organisations to track, measure, monitor and manage their Scope 3 emissions. The GHG protocol has specific categories as per their activities for accurate emission data and to avoid double-counting within an organisation under Scope 1, 2 and Scope 3.

Given the vast nature of the activities, not all 15 categories are applicable to a single organisation. For example, a manufacturing company will focus on fuel and energy-related activities, transportation and distribution, end-of-life treatment of sold products, and waste generated in operations. On the other hand, a logistics company will focus on transportation and distribution, purchased goods and services, and capital goods. This is why Scope 3 emission accounting mandates that organization only report emission that are relevant to them.

The GHG protocol standard divides Scope 3 emissions into upstream and downstream emissions on the basis of financial transactions of the reporting company.

Upstream emission activities

Upstream emissions are indirect GHG emissions that are related to purchased or acquired goods and services. Emissions under the upstream activities are associated with an organisation’s purchases that are carried out to ensure it swift flow of daily operations in terms of goods and services. All activities related to the company’s operations before a product is sent out fall under the upstream activities.

Downstream emission activities

Downstream emissions are indirect GHG emissions related to sold goods and services. The downstream emissions occur during the sale of the products and services by the reporting company.

The 15 categories of Scope 3 emissions

1. Purchased goods and services

This is category covers extraction, production and transportation of goods and services purchased or acquired by the organisation in the defined reporting year.

2. Capital goods

Organisations have to monitor emissions for extraction, production and transportation of capital goods purchased by the reporting company in the reporitng year.

3. Fuel- and energy-related activities (not included in Scope 1 or Scope 2)

This category covers the extraction, production and transportation of fuels and energy purchased by the reporting company during the reporting year. Four more categories of goods and services are included in this category. There are four different sub-categories of emissions:

- Upstream emissions of purchased fuels: This category involves emissions monitoring from extraction, production, and transportation of fuels consumed by the reporting company.

- Upstream emissions of purchased electricity: As the term itself suggests, the reporting company must monitor the emissions from extraction, production, and transportation of fuels consumed during the generation of electricity, steam, heating and cooling. This must be data and details of consumption by the reporting company.

- Transmission and distribution (T&D) losses: This data must be related to the generation of electricity, steam, heating and cooling lost by the reporting company.

- Generation of purchased electricity that is sold to end users: This is regarding the mintorirng of emissions from generation of electricity, steam, heating and cooling pucrchased by the reporting company and sold to end users.

4. Upstream transportation and distribution

This category covers the transportation and distribution of goods purchased by the reporting company during the reporting year between its tier 1 suppliers and its own operations. This applies for vehicles and facilities not owned by the reporting company. Under this category, inbound logictsics, outbound logistics , and transportation and distribution between a company’s own facilities are covered.

5. Waste generated in operations

Scope 3 emissions also take into account the disposal and treatment of waste generated during the reporting company’s operations in facilities not owned or not controlled by the organisation.

6. Business travel

Under this category, the transportation of employees for business-related activities during the reporting period is covered for vehicles not owned by the firm.

7. Employee commuting

This is related to the transportation of employees between their homes and their workplaces through vehicles not owned or operated by the reporting company.

8. Upstream leased assets

All activities of properties and assets leased by the reporting company during the reporting period year fall under this category. These must be the assets not included in the Scope 1 and Scope 2 emissions.

9. Downstream transportation and distribution

This is related to the transportation and distribution of products that are sold by the reporting company during the reporting year between the reporting company’s operations and the end consumer. This includes vehicles and facilities used for retail and storage but they are not owned or controlled by the reporting company.

10. Processing of sold products

In this category, the processing of intermediate products sold during the reporting year by downstream companies is covered.

11. Use of sold products

In this category, the end use of goods and services sold by the reporting company in the reporting year.

12. End-of-life treatment of sold products

The waste disposal and treatment of goods sold by the reporting company during the reporting year at the end of the products’ life.

13. Downstream leased assets

This category covers the emissions from the operation of assets owned by the reporting company. But these have to be leased to other entities in the reporting year.

14. Franchises

Activities of franchises during the reporting year that are not included in Scope 1 and Scope 2.

15. Investments

This category is about the operational investments during the reporting year. It includes equity and debt investments and project finance in the reporting year that are not included in Scope 1 and Scope 2.

Scope 3 emissions under SBTi

The Science Based Targets Initiatives (SBTi) says that companies must set Scope 3 targets to align with its criteria. The supplier engagement targets and reduction targets collectively cover at least 67% of total Scope 3 emissions. In a separate study titled SBTi research: Scope 3 discussion paper, about 4,205 companies and financial institutions had got their SBTi-validated targets by the end of 2023.

The SBTi maintains that monitoring and reporting targets must cover Scope 3 emissions if a company’s Scope 3 emissions account for more than 40% of the combined Scope 1,2 and 3 emissions.

How can organisations reduce their Scope 3 emissions?

There are multiple factors on which organisations depend while reducing Scope 3 emissions. Organisations must engage with their value chain through portals to collect primary data and improve Scope 3 emissions data accuracy. Moreover, firms must select the right emission factors from the available database. The success of accurate Scope 3 emissions accounting depends on the level of transparency while exchanging consistent, comparable, and credible Scope 3 emission data across value chains.

How The Sustainability Cloud helps in Scope 3 emissions accounting

Built on the global Scope 3 emissions accounting standards, TSC NetZero is helps organisations manage, measure and gather emissions data for all categories of Scope 3 emissions. It is software for all categories of Scope 3 value chain carbon accounting. It allows organisations to map their value chain’s carbon emissions through accurate activity-specific Scope 3 accounting with TSC NetZero. It ensures companies achieve Scope 3 emissions by improving accounting accuracy over time through accurate and regular reporting. Most importantly, TSC NetZero enables corporations to carry out primary and secondary data collection for all 15 activities using calculation methods.